Why should you buy the Malaysian Ringgit? Emerging market currencies have had a rough ride for the last 2 years due to global factors. Unfortunately, if you already owned the Malaysian ringgit then you had to ride out the volatility. However, for global investors the fluctuating currencies in emerging markets presents great opportunities.

The Malaysian Ringgit is one currency that presents great opportunity. The global winds of change have given ringgit holders a rough ride over the last couple of years. As a result, the ringgit is trading about 25-30% below historical valuations.

Factors forcing down the Malaysian ringgit include low oil prices, the strengthening of the US dollar, 1MDB uncertainty, sluggish global growth and the recent US presidential election. So as an investor you have got to ask yourself – what else could go wrong here? If the answer is hard to come up with then the ringgit may be at an inflection point.

Lets examine a few reasons why global investors should no longer neglect the Malaysian ringgit.

Oil Prices Effect Malaysian Ringgit

Starting in 2014 overproduction in the global oil industry finally came home to roost and the oil price plunged precipitously. Unfortunately, the Malaysian government is dependent on oil & gas revenues to fund their expenditures. As a result, the risk premium on their sovereign bonds increased and the ringgit depreciated.

However, the factors that are feeding this oil market weakness are short term and they should begin to rebalance by 2017-2018. Here is a short list of factors that will contribute to a rebalanced market.

- Due to the dearth of investment in the global oil sector we could see a global oil shortage in the next few years.

- International conflict is always a factor that can force oil production to come offline. Production in war torn Libya and Nigeria is already far below normal. Additionally, Venezuela is experiencing extreme levels of social unrest that could lower oil production levels.

- Global oil consumption continues to grow annually at over 1 million barrels per day.

- OPEC may agree to reinstate quotas and reduce supply which would provide short term relief.

When you add up these factors it indicates that the oil price weakness could blow over within 2-3 years. Until then, Malaysian Ringgit term deposits pay 4% interest which will help make it worth the wait.

Don’t forget that the price of oil is notoriously volatile and it wasn’t long ago that the price reached $140 per barrel! History tends to repeat itself and the factors that caused the last price spike are gradually re-emerging.

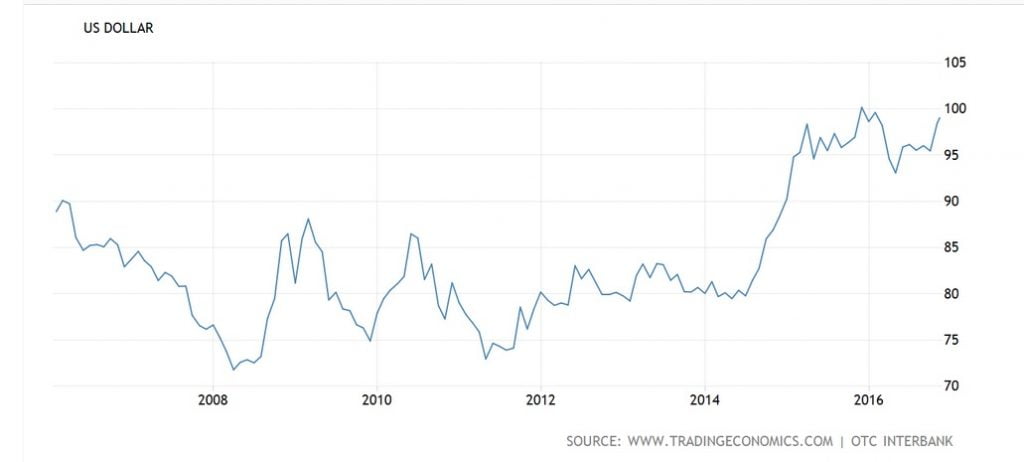

Historical Correlation of Global Oil & USD

The volatility in the price of oil and the USD have always had an inverse relationship. Ironically, in 2014 the USD started to rise and oil started to crash at almost exactly the same time!

10 Year History of Oil Prices

10 Year History US Dollar

As a result, this weak oil price means a strong US dollar and vice versa. The reason is that global oil sales are priced in USD. So when the US dollar weakens global oil consumption increases and pushes up the price, when the dollar strengthens oil becomes more expensive (outside the US) and oil consumption declines.

Therefore, when the oil market rebalances and the price of oil increases this should weaken the US dollar and help to relieve pressure on the Malaysian Ringgit.

Additional Factors Effecting USD vs Malaysian Ringgit

- The federal reserve has a dovish bias and is reticent to raise US interest rates above a nominal level. This is evident because there has been no rate increases in the US so far in 2016. Even if we do finally get the December 2016 rate increase, that is only a single .25% increase when the FOMC had projected a total of 4 rate increases for 2016.

- The lofty stock market valuations in the US are artificial because interest rates on corporate bonds are less than half what they historically would be. This deviation is caused because low/negative yielding sovereign bonds force investors to buy private corporate debt. The artificial demand forces down corporate debt servicing expenses and raises their bottom line. If the FOMC raises interest rates above a nominal level this will cause a sell off in corporate bonds and debt servicing costs will skyrocket. This will significantly lower stock market valuations and cause the US markets to crash. Thus, the Fed would need to reverse course and interest rates would simply go back to 0%.

- Relatively speaking the USD is massively overvalued. In 2006 short term interest rates were 5%, now they are .25%. Additionally, the debt to GDP in the US is over 2x what it was back in 2006. Plus, the US has a bunch of unfunded contingent liabilities such as social security and healthcare which are still unaccounted for. Yet the USD is trading higher than it was in 2006. In due time emerging market currencies such as the ringgit that have sustainable levels of government debt will strengthen.

1MDB Is Already Priced Into Malaysian Ringgit

The 1MDB scandal has shaken confidence in the Malaysian ringgit. However, the Malaysian economy had a total GDP of over $724 billion in 2014 and it is the 3rd largest economy in ASEAN. To put things in perspective, the entire 1MDB fund carries about $12 billion in debt. The funds in question that may have been misappropriated amount to 2-3 billion USD.

Proportionally speaking, the size of the 1MDB fund is insignificant compared to the larger Malaysian economy and government resources. Moreover, the Malaysian government has additional resources at its disposal such as Khazanah Nasional Berhad which is a sovereign wealth fund that had assets valued at over $150 billion in 2015. Therefore, the market reaction related to 1MDB is overdone and should begin to subside soon.

Global Trade Effect On Malaysian Ringgit

Unfortunately for the global economy, Donald Trump was elected on an anti globalization platform. The implications are that trade agreements such as TPP and NAFTA are dead in the water. Additionally, the US dollar could continue to strengthen because the FOMC will hasten their interest rate increases since Trump’s fiscal spending plans are considered inflationary.

Prolonged dollar strength and restrictions on global trade can cause problems for emerging markets that depend on the US. However, the president elect still has to get his anti trade policies through the US congress. This means that trade agreements such as TPP can still be renegotiated and may be revived after the hoopla surrounding the election subsides.

Additionally, Trump’s fiscal spending plans also need to get through the US congress to be approved. This could prove difficult because many of the newly elected Republicans in both houses are committed to a reduction in fiscal spending – not an increase! Either way, the FOMC will be very hesitant to raise interest rates due to the reasons previously mentioned.

US Trade Deficit Unsustainable

Either way, it is time for countries that have been placing undue reliance on the US to rethink their strategies. Indeed, if countries such as China, Japan and South Korea were not funding the huge Asian trade imbalance with the US, the purchasing power of the US consumer would be severely reduced. Most certainly, the fiscal sustainability of the US cannot be propped up indefinitely and trading partners of the US would be wise to make contingency plans.

Implications of US Bankruptcy For Malaysian Ringgit

President Elect Trump stated the obvious during his campaign, that the debt load of the US government was unsustainable. However, this certainly does not mean that the US will begin to live within its means and start to pay down the national debt. In fact quite the contrary, the global economy should be preparing for an improvised US bankruptcy proceeding.

Indeed, it will not be long before the US will stop kicking the can down the road and restructure their debt. This would result in a lot of market volatility and a swift devaluation of the US dollar. Countries with debt denominated in the US currency would benefit from the devaluation, but their economies may suffer at first because the purchasing power of the US consumer would be heavily diminished.

Additionally, countries holding large amounts of US treasuries such as China, Japan and South Korea would be well advised to taper future purchases.

Checkered History of Trump Business Empire

Donald Trump’s checkered business history contains 4 bankruptcies and therefore he is certainly an insolvency expert. In fact, bankruptcy is the secret behind his success, just ask the poor saps that invested in his Atlantic City casinos.

Unfortunately, there are no respectable investment insights to be found in his checkered past. Indeed, he is just another baby boomer that has been caught wrong footed during every US boom and bust cycle.

Why should US trade partners expect anything different to come about? Although I suspect he would try to get his fiscal programs implemented before he pulls the rug out from under US creditors.

Conclusion

The strength in the US dollar is transitory and repricing is very likely in short term at best or mid term at the worst. As a result, the Malaysian Ringgit and several other emerging market currencies should begin to recover soon.

Recommended Malaysia Travel Posts

Batu Caves in Selangor, Malaysia

Langkawi the “Jewel” of Malaysia

Dragon Boat Festival in Teluk Bahang